FDIC-Insured – Backed by the full faith and credit of the U.S. Government

Frequently Asked Questions

Quickly find the answers you need about our products, services and more.

FDIC-Insured – Backed by the full faith

and credit of the U.S. Government

and credit of the U.S. Government

Frequently Asked Questions

Quickly find the answers you need about our products, services and more.

FDIC-Insured – Backed by the full faith

and credit of the U.S. Government

and credit of the U.S. Government

Frequently Asked Questions

Quickly find the answers you need about our products, services and more.

Review Our FAQs

If you need additional information, please contact us or visit a branch and we’ll be happy to help!

General

After you open your First Midwest Bank checking account, you will receive our routing number and your account number. If your employer participates in a direct deposit program, simply provide this information to the payroll department at your company and your direct deposit will usually begin within 30 days.

Yes, you can order checks for your First Midwest Bank account online. Visit Deluxe, our secure third-party provider, to choose your design and easily order personalized checks in minutes.

Order Checks

To rent a safe deposit box from First Midwest Bank, visit one of the branches listed below that offers safe deposit boxes to sign a contract and receive your box and keys.

No, the contents of your safe deposit box are not covered by FDIC insurance. Your safe deposit box is strictly a storage space provided by First Midwest Bank in a secured vault.

Loans

- If you are interested in applying for a personal loan, debt consolidation loan, auto loan, or recreational vehicle loan, please contact one of our consumer lenders to schedule an appointment. You may also download an application and bring your completed application to apply in person at your local branch.

- If you are interested in applying for a home loan, construction loan, home improvement loan, or home equity line of credit, please contact one of our mortgage lenders to schedule an appointment, or – for all loans except HELOCs – apply online. You may also download an application and bring your completed application to apply in person at your local branch.

- If you are interested in applying for a commercial loan, line of credit, SBA loan, or agriculture loan, please contact one of our commercial lenders to schedule an appointment. You may also download an application and bring your completed application to apply in person at your local branch.

Please contact your local branch or call our Customer Service team at (573) 785-8461 for more information about our rates.

Yes, you may complete the loan preapproval process by providing the required documentation to verify your income, debts, and assets prior to your purchase. Once we obtain your credit report, we can make a credit-only loan decision.

Title insurance protects the lender (lender’s policy) and the homeowner (owner’s policy) against loss resulting from disputes over ownership of the property. Title insurance also lists any current liens against the property and current tax information.

Deposits and Savings

We offer Statement Savings, Christmas Club and Kids Club accounts, Health Savings Accounts, Money Market accounts, and Certificates of Deposit. If you would like further information, please call our Customer Service team at (573) 785-8461.

Open an Account

Minimum deposits are:

- $5 for Kids Club

- $5 for Christmas Club

- $50 for Checking

- $100 for Savings

- $1,000 for Money Market

All First Midwest Bank checking, savings, and money market accounts are eligible to receive free electronic statements. Since eStatements are delivered, viewed, and stored with our secure Online Banking solution, they are more secure than traditional statements delivered via U.S. Mail.

Yes, each individual customer’s account is insured by the FDIC up to $250,000 per depositor. First Midwest Bank customers also have access to insurance coverage on balances above FDIC limits for multimillion-dollar CD and/or money market deposit accounts.

Overdraft Education

An overdraft occurs when your account does not have enough money to cover a transaction. Overdrafts can happen when you:

- Write a check

- Withdraw money from an ATM

- Make an automatic bill payment

- Use your ATM/debit card to make a purchase

- Make an online banking transaction

When you overdraw your account, First Midwest Bank has the choice to either pay or not pay the transaction. We authorize and pay overdrafts on checks and automatic bill payments at our discretion.

- If we pay the amount, you will be charged an overdraft fee of $25 for each overdraft item we pay, with a maximum charge of $150 per day charged.

- If we return your check or automatic payment without paying it, you will be charged a non-sufficient funds (NSF) fee of $25.

- Sometimes the company or person to whom you wrote the check (store, utility company, etc.) may charge you a “returned check” fee in addition to the fee we may charge.

Accounts will be charged the standard overdraft fee of $25 for handling each overdraft created by check, ACH, point-of-sale, ATM withdrawal, in-person withdrawal, or other electronic item that is paid. For returned items, a standard fee of $25 will apply. An overdrawn balance must be brought positive within 35 days. We may not pay items under your overdraft privilege if you do not maintain your account in good standing by bringing your account to a positive balance within every 35-day period for a minimum of 24 hours, if you default on any loan or other obligation to First Midwest Bank, or if your account is subject to any legal or administrative order or levy.

You must opt in to our overdraft services in order for us to pay for these types of transactions. We pay overdrafts at our discretion, so we cannot guarantee that we will always authorize and pay any type of transaction.

Opt In or Opt Out

We know that it is easy to lose track of your balance, and we understand that anyone can make a mistake with their checking account – like forgetting when a previously scheduled automatic payment will occur. But what happens when you go to the gas station or grocery store and your card is denied because there isn’t enough money in your checking account?

By opting in and giving us permission to authorize and pay overdrafts on ATM or everyday debit card transactions, you can prevent the potential embarrassment and inconvenience of your transaction being declined.

Opt In or Opt Out

First Midwest offers Overdraft Privilege Service and Overdraft Protection Sweep. These plans do not have annual fees. So, if funds are not readily available in your account, our Overdraft Service plans give you flexibility and save you from having to pay overdraft fees.

You may be eligible for a $100 Overdraft Privilege Service at the time your account is opened, which will be reviewed with you during the application process.

- This Privilege amount enables the bank to pay any debits (up to $100) on your account that would cause your account to be overdrawn. An overdraft fee of $25 will be charged for each item paid. As always, the payment of overdrafts is at the bank’s discretion.

- After 35 days of the account being opened, a review will be conducted by the bank. If the account is determined to be in good standing and the Overdraft Privilege Service is not being used excessively, the account may qualify for a higher Privilege amount of up to $500.

- Following an overdraft, if your account is not brought to a positive balance within 35 days the bank will suspend your Overdraft Privilege.

You can ask us to link your checking account to your savings, money market, or another checking account. If you overdraw your checking account, we automatically transfer funds from the linked accounts to cover the shortage, assuming you have sufficient funds in the linked accounts.

Per federal regulation, there is a maximum of six preauthorized or automatic transfers per cycle that can be made on a statement savings or money market account.

The best way to avoid overdraft and NSF fees is to manage your account so that you do not overdraw it.

- Know how much money you have in your account by keeping track of your checks, automatic bill payments, and ATM/debit card transactions. Make sure to check your balance frequently, as it takes some checks and payments a few days to clear. The following services are available 24/7 for your convenience:

- Online Banking

- Mobile Banking

- iTalk Telephone Banking

- Review your account statements each month.

- You can set alerts through Online Banking or Mobile Banking to notify you when your account balance drops below the amount you specify. That way, you can transfer or deposit money to avoid overdrawing your account.

- If you do overdraw your account, deposit money into your account as soon as possible to cover the overdrawn amount plus any fees. This will help you avoid additional overdrafts and fees.

Online Banking

It only takes a few minutes to register for Online Banking. There are three ways to sign up:

- Enroll online or in the First Midwest Mobile Banking app

- Call our Customer Service team at (573) 785-8461

- Visit a branch

Online Banking is fast, easy, available 24/7, and best of all – it’s FREE! You can:

- View your current balance and all transactions for the past 30 days

- Create a budget and track spending

- Pay bills and schedule automatic payments

- Transfer funds to or from your First Midwest accounts without a fee

- Send money to family and friends

- Download your information to Quicken and QuickBooks

First Midwest Bank is committed to providing safe online banking services and keeping your financial information secure and confidential at all times. Whenever personal information is requested or displayed on our website, we use encryption technology, such as Secure Socket Layer (SSL), to prevent unauthorized access to data.

Mobile Deposit

Mobile Deposit is a convenient feature available within our Mobile Banking app. You can use your smartphone or tablet to submit photos of the front and back of your endorsed check and make a deposit directly into your eligible checking or savings account. Checks are not stored on your mobile device.

A customer is eligible to use Mobile Deposit once an account has been open for at least 90 days.

- You must be enrolled in First Midwest Online Banking.

- You must have the First Midwest Mobile Banking app installed on your mobile device (iPad, iPhone or Android).

- You must have no more than three returned payments in the last three months.

Yes, the online transmission of checks is secured through a secure SSL encrypted browser session. You should always protect your login and password for your Mobile Banking app and remember to log out completely when you finish using the Mobile Banking app, for added security.

Yes, Check 21 legislation allows banks to exchange images of checks for collection instead of paper. In fact, the majority of checks in the U.S. are cleared electronically today.

Mobile Deposit is free for all First Midwest Bank customers who meet all the eligibility requirements listed above.

- Other fees may still apply, however, such as those for returned items or overdrafts, per-item charges, limits on the number of items to deposit, and mobile carrier fees.

- You should also consult the bank’s fee schedule and deposit account agreement for further information regarding fees applicable to your account.

- Message and data rates may apply. Please check with your communications service provider for access rates, texting charges, and other applicable fees.

You will receive a deposit notification via email when your deposit is submitted. The deposit will be subject to verification and the bank’s Funds Availability Policy.

- All First Midwest Mobile Deposits made before 4:00 p.m. CST are processed and credited that evening and generally available on the next business day under the bank’s Funds Availability Policy.

- Items deposited after 4:00 p.m. CST will be processed the following business day, with availability of funds on the business day following when the deposit is processed.

- Deposits made on Saturday or throughout the weekend are processed on the next business day following that weekend. Saturdays, Sundays, and federal holidays are not considered business days for processing purposes, even if the bank may be open on those days.

Each check is considered a separate deposit. Checks must be endorsed “For Deposit Only to FMB” and with the owner’s signature.

- You can make up to 10 deposits in one day as long as the total amount deposited does not exceed $2,500.

- You can make up to 20 deposits in one month as long as the total amount deposited does not exceed $5,000.

We recommend you mark your check as being electronically deposited once it is submitted and processed. You should keep deposited checks for 60 days before destroying them.

Checks made payable to the account owner or joint owners that have been properly endorsed with the owner’s signature and “For Deposit Only to FMB.”

The following items cannot be deposited:

- Checks payable to any person or entity other than the person or entity that owns the account that the check is being deposited into

- Checks containing an alteration on the front of the check or item, or which you know or suspect, or should know or suspect, are fraudulent or otherwise not authorized by the owner of the account on which the check is drawn

- Checks payable jointly, unless deposited into an account in the name of all payees

- Checks previously converted to a substitute check, as defined in Reg. CC

- Checks drawn on a financial institution located outside the United States

- Checks that are remotely created checks, as defined in Reg. CC

- Checks not payable in United States currency

- Checks dated more than six months prior to the date of deposit

- Checks or items prohibited by the bank’s current procedures relating to the services or which are otherwise not acceptable under the terms of your account

- Checks with any endorsement on the back other than that specified in this agreement

- Checks that have previously been submitted through First Midwest Bank’s Mobile Deposit service or through a remote deposit capture service offered at any other financial institution

- Checks that have previously been deposited or negotiated in any way via any method at First Midwest Bank or any other

financial institution - Foreign checks

- Savings bonds

- Returned or re-deposited checks

- Rebate checks

- Note: The cutoff time for submitting deposits is 4:00 p.m. CST (Monday through Friday). First Midwest reserves the right to disable mobile app deposit capabilities.

iTalk Telephone Banking

Reach First Midwest Bank’s toll-free iTalk Telephone Banking line by calling (877) 824-4897. The system’s default is touch-tone. To activate speech recognition, press 2 after the greeting. You will be directed to the Main Menu. To access any account information, please have your account number and personal identification number (PIN) ready.

Menu Controls

- Main Menu, 3*

- Operator, 0

- Go Back, *

- Repeat, #

The system’s default is touch-tone. To activate speech recognition, press 2 after the greeting. Press or say the number with the options below to navigate the phone tree.

- Account Balance

Access account balances for any of the following:

- Checking Accounts

- Savings Accounts

- CD Accounts

- Loan Accounts

- Account History

- Last 5 Transactions

- Deposits

- Withdrawals

- Check Number

- Amount

- Date

- ATM Transactions

- Transfer Funds or Make a Payment

- Transfer Funds Immediately

- Schedule a Funds Transfer

- Payments

- Hear Existing Scheduled Transfers

- Delete an Existing Transfer

- Stop Payment Activities

- Stop a Payment

- Stop Payment Inquiry

- Change Your Access Code

- Change Overdraft Options

- Locations & Hours

Your member number is the same as your account number. Enter your account number when prompted, then wait for the prompt to enter your personal identification number (PIN).

From the Main Menu, press 1 for Account Balance. The Account Balance option provides both the current balance and available balance (your current balance minus any holds).

During regular business hours, press 0 at any point to reach a customer service representative.

You can search for transactions by type, check number, amount/range or date(s). To find out which transactions have cleared your account, go to the Main Menu, press 2 for Account History, then listen to the options.

You can change your personal identification number (PIN), but it must be a new number. You cannot reuse a PIN. To change your PIN, go to the Main Menu and press 5 to Change Your Access Code. If you haven’t used iTalk before, you will be prompted to select a PIN.

Checkbook Tools

With a little practice, writing checks is easy. When you write a check, always use a blue or black ink pen and write neatly. It is important to write your check legibly to make sure your check is accurately processed.

Every time you write a check, you’ll fill in the following six areas:

- Date: Write the date (month, day and year).

- Pay to the Order of: Write the name of the check’s recipient.

- $ Amount: Write the check’s amount using numerals. When you write the number, start at the left and don’t leave any blank space, to prevent someone else from adding more numbers.

- Dollars: Write, in words, how much the check is for. When you write the words for the dollars, start at the left side. Write any cents as a fraction. (See sample.) Draw a line through the extra space.

- Signature: Sign your name on the signature line, just like it appears on the top of the check. Don’t sign the check until you are ready to use it. If you sign it ahead of time, someone else could use the check.

- Memo: Note what the payment is for.

To deposit a check, you need to endorse it first. That means you sign your name in ink on the back of the check. Sign your name the same way it’s written on the check. If your name is spelled wrong, also sign your name the correct way on the next line.

You can endorse your check three different ways:

- Blank Endorsement

Sign your name the same way it’s written on the front of the check. Only sign it when you’re ready to cash it or deposit the money into your account. Once the check is signed on the back (endorsed), someone else could get your money if you lose the check.

- Special Endorsement

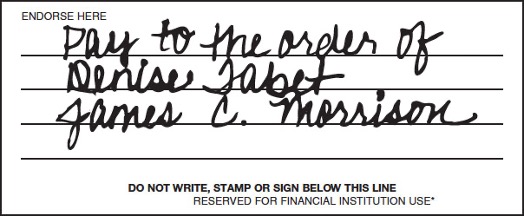

Do this when you want to give someone else the money. Write “Pay to the order of” and that person’s name below it. Then sign your name underneath. Now only that person can cash the check.

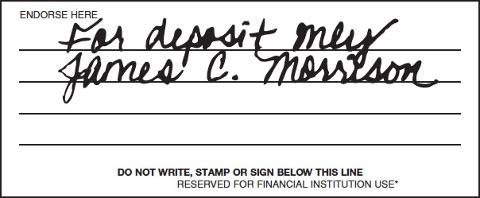

- Restrictive Endorsement

When you want to take extra precautions with your check, such as when you send it to First Midwest Bank or another financial institution in the mail, use this kind of endorsement. Write “For deposit only” and sign your name underneath. Now the check can only be deposited into your account, not cashed.

- Keep all your checks in a safe place. Checks can be stolen and used by other people, just like cash. If your checks are ever lost or stolen, contact us immediately!

- Put the right date (month, day and year) on your checks.

- Sign your name like it’s printed on the check. Use blue or black ink and write neatly.

- Keep track of your ATM withdrawals and debit card transactions to make sure you have enough money in your account to pay the

check amount.

- Don’t write checks for more money than you have in your account. When this happens, financial institutions refer to it as “non-sufficient funds” (NSF). You may have heard it called “bouncing a check” or “writing a bad check.”

- Here is what can happen if you write checks without enough money in your First Midwest Bank account:

- You could be charged an overdraft fee by First Midwest Bank.

- The merchant to which you wrote the “bad” check could charge you another fee.

- The merchant to which you wrote the “bad” check could decide not to take your checks in the future.

- Your name could go on a risk check or “risk credit” list, and other financial institutions won’t take your checks.

- Your checking account could be closed by First Midwest Bank and you won’t be allowed to write any checks at all. We may report this information to other financial institutions, and they may refuse to open a checking account for you for up to seven years after your account was closed.

- You could get letters and phone calls from the people you owe the money to.

- Don’t sign blank checks. They can be stolen and used by someone else.

- Don’t erase mistakes on a check. Either write VOID across the entire check and next to its number in the check register and tear up the check, or fix the mistake on the check and write your initials next to the mistake.

- Don’t use other people’s checks or let them use yours.

- Don’t use a pencil. People can erase the numbers when you write in pencil. Always use a blue or black ink pen.

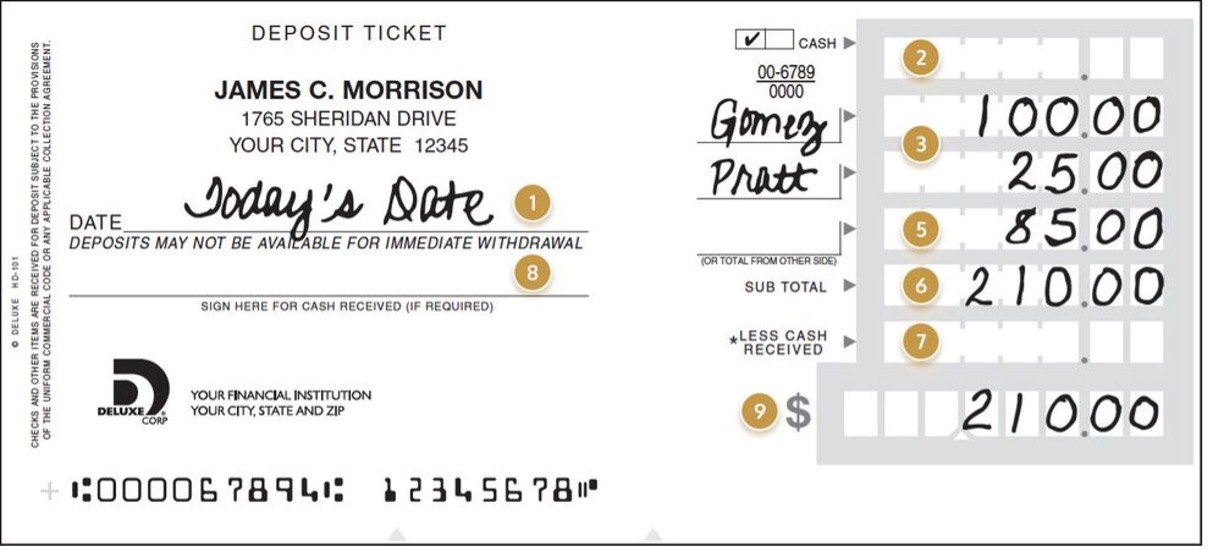

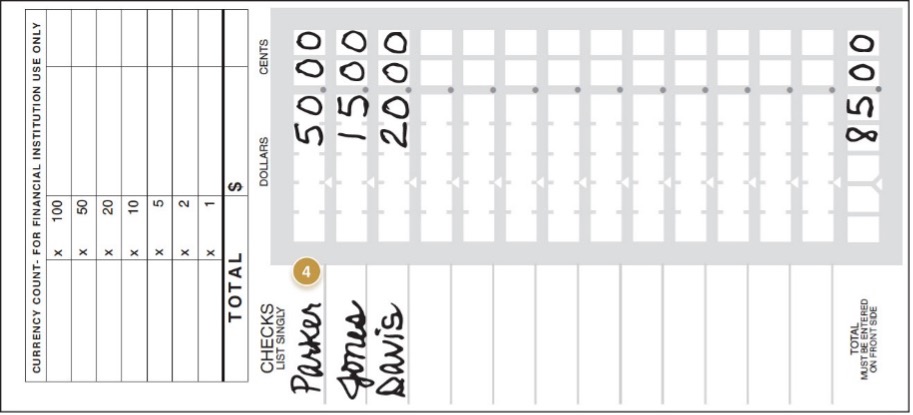

You can deposit cash and checks into your account in different ways. When you’re ready to deposit money at First Midwest Bank, you need to fill out a form called a deposit ticket. You’ll find your deposit tickets in your checkbook, behind the checks. They have printing on both sides. Just like with the checks and the check register, there are areas you need to complete. Use a blue or black ink pen to fill out the form. It is very important that you write neatly.

Here are the spots to fill in on your deposit ticket:

- Date: The date (month, day and year) that you are making the deposit.

- Cash: The total amount of cash you are depositing.

- Check Entry Area: This is where you write down each check you’re depositing. Put each check amount on its own line.

- Additional Check Entry Area: If you run out of room on the front, the back of the deposit ticket also has space for checks.

- Total From Other Side: If you have more than three checks and wrote them down on the back side, add them up and put the total amount here. If you are depositing three checks, this is the place you write down the third one.

- Sub Total: Add lines 2, 3 and 5.

- Less Cash Received: If you want to deposit part of the money, and get part of the money in cash, write down how much you want to receive in cash.

- Sign Here: If you want cash back, sign your name here.

- Net Deposit: Add all the cash and all the checks together. If you are receiving cash back, subtract that amount. The result is your net deposit. Write down that amount here.Front:

Back:

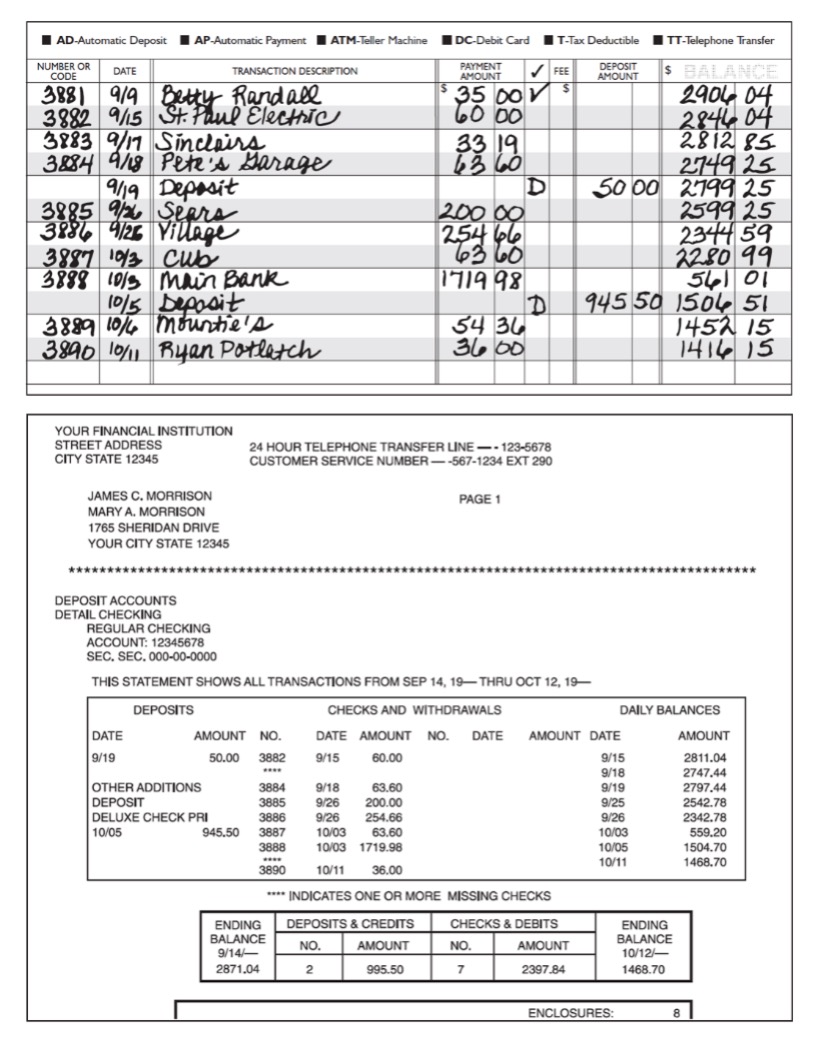

Every month, you’ll get a statement from First Midwest Bank. You may receive a paper statement in the mail, or you may access an electronic statement in Online Banking. This statement tells you:

- Every check that you wrote (the ones that have been processed)

- Money you took out of the ATM, transferred by telephone or any other withdrawals

- All of your debit card transactions

- All of your deposits

- Your ending balance (how much you have in your account on the date the statement was issued)

In this section we’ll explain how to keep accurate records. The first thing we’ll cover is how to reconcile your accounts to see how much you deposited into your account, how much you spent, and how much you have left. To reconcile your account, you need to look at your check register and your statement together and compare them. Here’s how to start:

- First, open the envelope with your statement or log in to Online Banking to access your electronic statement. If you receive your statement in the mail, your canceled checks may also be in the envelope. Many financial institutions keep the real checks and return a list or picture image of your check or substitute check on your statement.

- If you get your checks back, put them in order according to the check number.

- Look at your statement and find the first check number listed.

- Look at your check register. Find that same check number and place a check mark in the column labeled (√ or “Code*”). Do this for every check on your statement.

- Complete steps 3 and 4 above for every deposit. Check it off on your statement and check it off on your register.

- If you see checks in your check register that are not listed on the statement, that means they have not cleared yet. Don’t check them off. They will be listed on a future statement.

- If you have any other service fees or charges for checks, ATM withdrawals, financial institution services or automatic deductions (such as a car loan payment) listed on your statement, write them in your check register. Don’t forget to subtract those charges from your balance in your check register.

- If First Midwest Bank pays interest on your checking account, add the interest amount to your check register.

- Now your checkbook should be up to date.

Most of the time, your checkbook balance and the statement won’t match. That is normal. This usually happens because of outstanding checks and any deposits or withdrawals that you made after the statement was printed.

Your statement will include a reconciliation form (usually on the back) to help you reconcile your account. Here’s how to use it:

- List deposits, checks and other withdrawals that you have written in your check register, but are not listed on the statement in the proper columns.

- Write down the total amount of the deposit list and the checks/withdrawals list.

- Write down the ending balance printed on the front of your statement.

- Enter the total deposits from line 2. Add lines 3 and 4 and enter that amount on the subtotal line.

- Enter the total withdrawals from line 2 and subtract that amount from the subtotal.

- Now the balance of your checkbook should match the ending balance on your statement.

A check register helps you keep track of the money in your checking account. That’s where you write down everything you do with your account. Whenever you deposit money or withdraw money, or use your ATM or debit card, write it in the check register immediately. When you write something in your check register, that’s known as recording a transaction.

The top of the check register has the following transaction codes:

- ATM: Automatic Teller Machine

- D: Deposit

- DC: Debit Card

- E: Electronic Check

- TT: Telephone Transfer

- T: Tax Deductible

- O: Other

- Number: This is the check number. You’ll find it in the upper right corner of each check. Every check has a different sequential number.

- Date: Write the date you wrote the check.

- Description of Transaction: Describe your transaction here. Examples include: deposit money, check for groceries, ATM withdrawal, debit card purchase or transfer funds.

- Payment/Debit: Write the check or withdrawal amount.

- Code for Transaction: This is where you fill in a code for the transactions you make when you aren’t writing a check. When you get your statement, every month you’ll place a “√” through this box when you see the transaction listed.

- Service Fee: If you are charged a fee to withdraw money from the ATM, write that amount in this space.

- Deposit/Credit: Did you deposit money into your account or receive a credit from a merchant? Write down any deposit amounts into your account.

- Balance: To find out how much money you have, add the deposited money to what you had before. Or subtract the withdrawal amount from what you had before. The money left is your balance.

Automated Teller Machine (ATM): Also known as the money machine or cash machine.

Bad Check: A check that is written when there is not enough money in the account. Also known as a bounced check.

Balance: The amount of money you have in your account.

Cash: Money in the form of bills or coins.

Check: A document used for payment.

Check 21: Federal legislation passed in 2004 that permits financial institutions to create and submit substitute checks from electronic images for processing.

Check Register: A form to keep track of your checking account transactions.

Checking Account: A payment method to manage your money efficiently.

Cleared Check: A check that has gone through the financial institution’s processing center and is listed on your monthly statement.

Debit Card: A card that can be used at an ATM or merchant. Unlike a credit card, the funds are deducted from your checking account.

Deposit: The money you put into your account or the act of putting money into your account.

Deposit Ticket: The form you use to put money into your account.

Electronic Check: When you write a check to a merchant and the merchant hands the check back to you. The check is converted to an automatic deduction to your checking account.

Endorse: To sign your name on the back of a check in order to cash it or deposit it.

Financial Institution: An establishment that completes and facilitates money transactions, such as a bank or credit union.

Less Cash Received: The amount of cash you get back when you make a deposit.

Memo: The area on a check that notes what the check was written to pay for.

Non-sufficient Funds: When you do not have enough money in your account to cover a check, debit card purchase or other transaction.

Non-sufficient Funds Fee: The fee that is charged by a financial institution or business when a check does not clear or there isn’t enough money in your account to cover a transfer or withdrawal.

Outstanding Check: A check that is still going through financial institution processing.

Overdraft: When your account goes below zero and there is not enough money to cover the withdrawal.

Reconcile: A process to make sure your checkbook balance matches your financial institution’s balance for your account.

Reconciliation: When you have verified that your checkbook balance is the same as your financial institution’s balance for your account.

Reconciliation Form: A form that helps you reconcile your account. See Reconcile.

Recording a Transaction: The act of writing down a transaction in your check register. See Transaction.

Statement: The documentation you get every month from your financial institution that lists all of the activities in your account

for the month. Transaction: When money goes into, or out of, your account. Transactions can include deposits, withdrawals, payments, fees, ATM transactions or transfers.

for the month. Transaction: When money goes into, or out of, your account. Transactions can include deposits, withdrawals, payments, fees, ATM transactions or transfers.

Review Our FAQs

If you need additional information, please contact us or visit a branch and we’ll be happy to help!

General

After you open your First Midwest Bank checking account, you will receive our routing number and your account number. If your employer participates in a direct deposit program, simply provide this information to the payroll department at your company and your direct deposit will usually begin within 30 days.

Yes, you can order checks for your First Midwest Bank account online. Visit Deluxe, our secure third-party provider, to choose your design and easily order personalized checks in minutes.

Order Checks

To rent a safe deposit box from First Midwest Bank, visit one of the branches listed below that offers safe deposit boxes to sign a contract and receive your box and keys.

No, the contents of your safe deposit box are not covered by FDIC insurance. Your safe deposit box is strictly a storage space provided by First Midwest Bank in a secured vault.

Loans

- If you are interested in applying for a personal loan, debt consolidation loan, auto loan, or recreational vehicle loan, please contact one of our consumer lenders to schedule an appointment. You may also download an application and bring your completed application to apply in person at your local branch.

- If you are interested in applying for a home loan, construction loan, home improvement loan, or home equity line of credit, please contact one of our mortgage lenders to schedule an appointment, or – for all loans except HELOCs – apply online. You may also download an application and bring your completed application to apply in person at your local branch.

- If you are interested in applying for a commercial loan, line of credit, SBA loan, or agriculture loan, please contact one of our commercial lenders to schedule an appointment. You may also download an application and bring your completed application to apply in person at your local branch.

Please contact your local branch or call our Customer Service team at (573) 624-3571 for more information about our rates.

Yes, you may complete the loan preapproval process by providing the required documentation to verify your income, debts, and assets prior to your purchase. Once we obtain your credit report, we can make a credit-only loan decision.

Title insurance protects the lender (lender’s policy) and the homeowner (owner’s policy) against loss resulting from disputes over ownership of the property. Title insurance also lists any current liens against the property and current tax information.

Deposits and Savings

We offer Statement Savings, Christmas Club and Kids Club accounts, Health Savings Accounts, Money Market accounts, and Certificates of Deposit. If you would like further information, please call our Customer Service team at (573) 624-3571.

Open an Account

Minimum deposits are:

- $5 for Kids Club

- $5 for Christmas Club

- $50 for Checking

- $100 for Savings

- $1,000 for Money Market

All First Midwest Bank checking, savings, and money market accounts are eligible to receive free electronic statements. Since eStatements are delivered, viewed, and stored with our secure Online Banking solution, they are more secure than traditional statements delivered via U.S. Mail.

Yes, each individual customer’s account is insured by the FDIC up to $250,000 per depositor. First Midwest Bank customers also have access to insurance coverage on balances above FDIC limits for multimillion-dollar CD and/or money market deposit accounts.

Overdraft Education

An overdraft occurs when your account does not have enough money to cover a transaction. Overdrafts can happen when you:

- Write a check

- Withdraw money from an ATM

- Make an automatic bill payment

- Use your ATM/debit card to make a purchase

- Make an online banking transaction

When you overdraw your account, First Midwest Bank has the choice to either pay or not pay the transaction. We authorize and pay overdrafts on checks and automatic bill payments at our discretion.

- If we pay the amount, you will be charged an overdraft fee of $28 for each overdraft item we pay, with a maximum charge of $168 per day charged.

- If we return your check or automatic payment without paying it, you will be charged a non-sufficient funds (NSF) fee of $28.

- Sometimes the company or person to whom you wrote the check (store, utility company, etc.) may charge you a “returned check” fee in addition to the fee we may charge.

Accounts will be charged the standard overdraft fee of $28 for handling each overdraft created by check, ACH, point-of-sale, ATM withdrawal, in-person withdrawal, or other electronic item that is paid. For returned items, a standard fee of $28 will apply. An overdrawn balance must be brought positive within 35 days. We may not pay items under your overdraft privilege if you do not maintain your account in good standing by bringing your account to a positive balance within every 35-day period for a minimum of 24 hours, if you default on any loan or other obligation to First Midwest Bank, or if your account is subject to any legal or administrative order or levy.

You must opt in to our overdraft services in order for us to pay for these types of transactions. We pay overdrafts at our discretion, so we cannot guarantee that we will always authorize and pay any type of transaction.

Opt In or Opt Out

We know that it is easy to lose track of your balance, and we understand that anyone can make a mistake with their checking account – like forgetting when a previously scheduled automatic payment will occur. But what happens when you go to the gas station or grocery store and your card is denied because there isn’t enough money in your checking account?

By opting in and giving us permission to authorize and pay overdrafts on ATM or everyday debit card transactions, you can prevent the potential embarrassment and inconvenience of your transaction being declined.

Opt In or Opt Out

First Midwest offers Overdraft Privilege Service and Overdraft Protection Sweep. These plans do not have annual fees. So, if funds are not readily available in your account, our Overdraft Service plans give you flexibility and save you from having to pay overdraft fees.

You may be eligible for a $100 Overdraft Privilege Service at the time your account is opened, which will be reviewed with you during the application process.

- This Privilege amount enables the bank to pay any debits (up to $100) on your account that would cause your account to be overdrawn. An overdraft fee of $28 will be charged for each item paid. As always, the payment of overdrafts is at the bank’s discretion.

- After 35 days of the account being opened, a review will be conducted by the bank. If the account is determined to be in good standing and the Overdraft Privilege Service is not being used excessively, the account may qualify for a higher Privilege amount of up to $500.

- Following an overdraft, if your account is not brought to a positive balance within 35 days the bank will suspend your Overdraft Privilege.

You can ask us to link your checking account to your savings, money market, or another checking account. If you overdraw your checking account, we automatically transfer funds from the linked accounts to cover the shortage, assuming you have sufficient funds in the linked accounts.

Per federal regulation, there is a maximum of six preauthorized or automatic transfers per cycle that can be made on a statement savings or money market account.

The best way to avoid overdraft and NSF fees is to manage your account so that you do not overdraw it.

- Know how much money you have in your account by keeping track of your checks, automatic bill payments, and ATM/debit card transactions. Make sure to check your balance frequently, as it takes some checks and payments a few days to clear. The following services are available 24/7 for your convenience:

- Online Banking

- Mobile Banking

- iTalk Telephone Banking

- Review your account statements each month.

- You can set alerts through Online Banking or Mobile Banking to notify you when your account balance drops below the amount you specify. That way, you can transfer or deposit money to avoid overdrawing your account.

- If you do overdraw your account, deposit money into your account as soon as possible to cover the overdrawn amount plus any fees. This will help you avoid additional overdrafts and fees.

Online Banking

It only takes a few minutes to register for Online Banking. There are three ways to sign up:

- Enroll online or in the First Midwest Mobile Banking app

- Call our Customer Service team at (573) 624-3571

- Visit a branch

Online Banking is fast, easy, available 24/7, and best of all – it’s FREE! You can:

- View your current balance and all transactions for the past 30 days

- Create a budget and track spending

- Pay bills and schedule automatic payments

- Transfer funds to or from your First Midwest accounts without a fee

- Send money to family and friends

- Download your information to Quicken and QuickBooks

First Midwest Bank is committed to providing safe online banking services and keeping your financial information secure and confidential at all times. Whenever personal information is requested or displayed on our website, we use encryption technology, such as Secure Socket Layer (SSL), to prevent unauthorized access to data.

Mobile Deposit

Mobile Deposit is a convenient feature available within our Mobile Banking app. You can use your smartphone or tablet to submit photos of the front and back of your endorsed check and make a deposit directly into your eligible checking or savings account. Checks are not stored on your mobile device.

A customer is eligible to use Mobile Deposit once an account has been open for at least 90 days.

- You must be enrolled in First Midwest Online Banking .

- You must have the First Midwest Mobile Banking app installed on your mobile device (iPad, iPhone or Android).

- You must have no more than three returned payments in the last three months.

Yes, the online transmission of checks is secured through a secure SSL encrypted browser session. You should always protect your login and password for your Mobile Banking app and remember to log out completely when you finish using the Mobile Banking app, for added security.

Yes, Check 21 legislation allows banks to exchange images of checks for collection instead of paper. In fact, the majority of checks in the U.S. are cleared electronically today.

Mobile Deposit is free for all First Midwest Bank customers who meet all the eligibility requirements listed above.

- Other fees may still apply, however, such as those for returned items or overdrafts, per-item charges, limits on the number of items to deposit, and mobile carrier fees.

- You should also consult the bank’s fee schedule and deposit account agreement for further information regarding fees applicable to your account.

- Message and data rates may apply. Please check with your communications service provider for access rates, texting charges, and other applicable fees.

You will receive a deposit notification via email when your deposit is submitted. The deposit will be subject to verification and the bank’s Funds Availability Policy.

- All First Midwest Mobile Deposits made before 3:00 p.m. CST are processed and credited that evening and generally available on the next business day under the bank’s Funds Availability Policy.

- Items deposited after 3:00 p.m. CST will be processed the following business day, with availability of funds on the business day following when the deposit is processed.

- Deposits made on Saturday or throughout the weekend are processed on the next business day following that weekend. Saturdays, Sundays, and federal holidays are not considered business days for processing purposes, even if the bank may be open on those days.

Each check is considered a separate deposit. Checks must be endorsed “For Deposit Only to FMB” and with the owner’s signature.

- You can make up to 10 deposits in one day as long as the total amount deposited does not exceed $2,500.

- You can make up to 20 deposits in one month as long as the total amount deposited does not exceed $5,000.

We recommend you mark your check as being electronically deposited once it is submitted and processed. You should keep deposited checks for 60 days before destroying them.

Checks made payable to the account owner or joint owners that have been properly endorsed with the owner’s signature and “For Deposit Only to FMB.”

The following items cannot be deposited:

- Checks payable to any person or entity other than the person or entity that owns the account that the check is being deposited into

- Checks containing an alteration on the front of the check or item, or which you know or suspect, or should know or suspect, are fraudulent or otherwise not authorized by the owner of the account on which the check is drawn

- Checks payable jointly, unless deposited into an account in the name of all payees

- Checks previously converted to a substitute check, as defined in Reg. CC

- Checks drawn on a financial institution located outside the United States

- Checks that are remotely created checks, as defined in Reg. CC

- Checks not payable in United States currency

- Checks dated more than six months prior to the date of deposit

- Checks or items prohibited by the bank’s current procedures relating to the services or which are otherwise not acceptable under the terms of your account

- Checks with any endorsement on the back other than that specified in this agreement

- Checks that have previously been submitted through First Midwest Bank’s Mobile Deposit service or through a remote deposit capture service offered at any other financial institution

- Checks that have previously been deposited or negotiated in any way via any method at First Midwest Bank or any other

financial institution - Foreign checks

- Savings bonds

- Returned or re-deposited checks

- Rebate checks

- Note: The cutoff time for submitting deposits is 3:00 p.m. CST (Monday through Friday). First Midwest reserves the right to disable mobile app deposit capabilities.

iTalk Telephone Banking

Reach First Midwest Bank’s toll-free iTalk Telephone Banking line by calling (877) 824-4913. The system’s default is touch-tone. To activate speech recognition, press 2 after the greeting. You will be directed to the Main Menu. To access any account information, please have your account number and personal identification number (PIN) ready.

Menu Controls

- Main Menu, 3*

- Operator, 0

- Go Back, *

- Repeat, #

The system’s default is touch-tone. To activate speech recognition, press 2 after the greeting. Press or say the number with the options below to navigate the phone tree.

- Account Balance

Access account balances for any of the following:

- Checking Accounts

- Savings Accounts

- CD Accounts

- Loan Accounts

- Account History

- Last 5 Transactions

- Deposits

- Withdrawals

- Check Number

- Amount

- Date

- ATM Transactions

- Transfer Funds or Make a Payment

- Transfer Funds Immediately

- Schedule a Funds Transfer

- Payments

- Hear Existing Scheduled Transfers

- Delete an Existing Transfer

- Stop Payment Activities

- Stop a Payment

- Stop Payment Inquiry

- Change Your Access Code

- Change Overdraft Options

- Locations & Hours

Your member number is the same as your account number. Enter your account number when prompted, then wait for the prompt to enter your personal identification number (PIN).

From the Main Menu, press 1 for Account Balance. The Account Balance option provides both the current balance and available balance (your current balance minus any holds).

You can search for transactions by type, check number, amount/range or date(s). To find out which transactions have cleared your account, go to the Main Menu, press 2 for Account History, then listen to the options.

During regular business hours, press 0 at any point to reach a customer service representative.

You can change your personal identification number (PIN), but it must be a new number. You cannot reuse a PIN. To change your PIN, go to the Main Menu and press 5 to Change Your Access Code. If you haven’t used iTalk before, you will be prompted to select a PIN.

Checkbook Tools

With a little practice, writing checks is easy. When you write a check, always use a blue or black ink pen and write neatly. It is important to write your check legibly to make sure your check is accurately processed.

Every time you write a check, you’ll fill in the following six areas:

- Date: Write the date (month, day and year).

- Pay to the Order of: Write the name of the check’s recipient.

- $ Amount: Write the check’s amount using numerals. When you write the number, start at the left and don’t leave any blank space, to prevent someone else from adding more numbers.

- Dollars: Write, in words, how much the check is for. When you write the words for the dollars, start at the left side. Write any cents as a fraction. (See sample.) Draw a line through the extra space.

- Signature: Sign your name on the signature line, just like it appears on the top of the check. Don’t sign the check until you are ready to use it. If you sign it ahead of time, someone else could use the check.

- Memo: Note what the payment is for.

To deposit a check, you need to endorse it first. That means you sign your name in ink on the back of the check. Sign your name the same way it’s written on the check. If your name is spelled wrong, also sign your name the correct way on the next line.

You can endorse your check three different ways:

- Blank Endorsement

Sign your name the same way it’s written on the front of the check. Only sign it when you’re ready to cash it or deposit the money into your account. Once the check is signed on the back (endorsed), someone else could get your money if you lose the check.

- Special Endorsement

Do this when you want to give someone else the money. Write “Pay to the order of” and that person’s name below it. Then sign your name underneath. Now only that person can cash the check.

- Restrictive Endorsement

When you want to take extra precautions with your check, such as when you send it to First Midwest Bank or another financial institution in the mail, use this kind of endorsement. Write “For deposit only” and sign your name underneath. Now the check can only be deposited into your account, not cashed.

- Keep all your checks in a safe place. Checks can be stolen and used by other people, just like cash. If your checks are ever lost or stolen, contact us immediately!

- Put the right date (month, day and year) on your checks.

- Sign your name like it’s printed on the check. Use blue or black ink and write neatly.

- Keep track of your ATM withdrawals and debit card transactions to make sure you have enough money in your account to pay the

check amount.

- Don’t write checks for more money than you have in your account. When this happens, financial institutions refer to it as “non-sufficient funds” (NSF). You may have heard it called “bouncing a check” or “writing a bad check.”

- Here is what can happen if you write checks without enough money in your First Midwest Bank account:

- You could be charged an overdraft fee by First Midwest Bank.

- The merchant to which you wrote the “bad” check could charge you another fee.

- The merchant to which you wrote the “bad” check could decide not to take your checks in the future.

- Your name could go on a risk check or “risk credit” list, and other financial institutions won’t take your checks.

- Your checking account could be closed by First Midwest Bank and you won’t be allowed to write any checks at all. We may report this information to other financial institutions, and they may refuse to open a checking account for you for up to seven years after your account was closed.

- You could get letters and phone calls from the people you owe the money to.

- Don’t sign blank checks. They can be stolen and used by someone else.

- Don’t erase mistakes on a check. Either write VOID across the entire check and next to its number in the check register and tear up the check, or fix the mistake on the check and write your initials next to the mistake.

- Don’t use other people’s checks or let them use yours.

- Don’t use a pencil. People can erase the numbers when you write in pencil. Always use a blue or black ink pen.

You can deposit cash and checks into your account in different ways. When you’re ready to deposit money at First Midwest Bank, you need to fill out a form called a deposit ticket. You’ll find your deposit tickets in your checkbook, behind the checks. They have printing on both sides. Just like with the checks and the check register, there are areas you need to complete. Use a blue or black ink pen to fill out the form. It is very important that you write neatly.

Here are the spots to fill in on your deposit ticket:

- Date: The date (month, day and year) that you are making the deposit.

- Cash: The total amount of cash you are depositing.

- Check Entry Area: This is where you write down each check you’re depositing. Put each check amount on its own line.

- Additional Check Entry Area: If you run out of room on the front, the back of the deposit ticket also has space for checks.

- Total From Other Side: If you have more than three checks and wrote them down on the back side, add them up and put the total amount here. If you are depositing three checks, this is the place you write down the third one.

- Sub Total: Add lines 2, 3 and 5.

- Less Cash Received: If you want to deposit part of the money, and get part of the money in cash, write down how much you want to receive in cash.

- Sign Here: If you want cash back, sign your name here.

- Net Deposit: Add all the cash and all the checks together. If you are receiving cash back, subtract that amount. The result is your net deposit. Write down that amount here.Front:

Back:

Every month, you’ll get a statement from First Midwest Bank. You may receive a paper statement in the mail, or you may access an electronic statement in Online Banking. This statement tells you:

- Every check that you wrote (the ones that have been processed)

- Money you took out of the ATM, transferred by telephone or any other withdrawals

- All of your debit card transactions

- All of your deposits

- Your ending balance (how much you have in your account on the date the statement was issued)

In this section we’ll explain how to keep accurate records. The first thing we’ll cover is how to reconcile your accounts to see how much you deposited into your account, how much you spent, and how much you have left. To reconcile your account, you need to look at your check register and your statement together and compare them. Here’s how to start:

- First, open the envelope with your statement or log in to Online Banking to access your electronic statement. If you receive your statement in the mail, your canceled checks may also be in the envelope. Many financial institutions keep the real checks and return a list or picture image of your check or substitute check on your statement.

- If you get your checks back, put them in order according to the check number.

- Look at your statement and find the first check number listed.

- Look at your check register. Find that same check number and place a check mark in the column labeled (√ or “Code*”). Do this for every check on your statement.

- Complete steps 3 and 4 above for every deposit. Check it off on your statement and check it off on your register.

- If you see checks in your check register that are not listed on the statement, that means they have not cleared yet. Don’t check them off. They will be listed on a future statement.

- If you have any other service fees or charges for checks, ATM withdrawals, financial institution services or automatic deductions (such as a car loan payment) listed on your statement, write them in your check register. Don’t forget to subtract those charges from your balance in your check register.

- If First Midwest Bank pays interest on your checking account, add the interest amount to your check register.

- Now your checkbook should be up to date.

Most of the time, your checkbook balance and the statement won’t match. That is normal. This usually happens because of outstanding checks and any deposits or withdrawals that you made after the statement was printed.

Your statement will include a reconciliation form (usually on the back) to help you reconcile your account. Here’s how to use it:

- List deposits, checks and other withdrawals that you have written in your check register, but are not listed on the statement in the proper columns.

- Write down the total amount of the deposit list and the checks/withdrawals list.

- Write down the ending balance printed on the front of your statement.

- Enter the total deposits from line 2. Add lines 3 and 4 and enter that amount on the subtotal line.

- Enter the total withdrawals from line 2 and subtract that amount from the subtotal.

- Now the balance of your checkbook should match the ending balance on your statement.

A check register helps you keep track of the money in your checking account. That’s where you write down everything you do with your account. Whenever you deposit money or withdraw money, or use your ATM or debit card, write it in the check register immediately. When you write something in your check register, that’s known as recording a transaction.

The top of the check register has the following transaction codes:

- ATM: Automatic Teller Machine

- D: Deposit

- DC: Debit Card

- E: Electronic Check

- TT: Telephone Transfer

- T: Tax Deductible

- O: Other

- Number: This is the check number. You’ll find it in the upper right corner of each check. Every check has a different sequential number.

- Date: Write the date you wrote the check.

- Description of Transaction: Describe your transaction here. Examples include: deposit money, check for groceries, ATM withdrawal, debit card purchase or transfer funds.

- Payment/Debit: Write the check or withdrawal amount.

- Code for Transaction: This is where you fill in a code for the transactions you make when you aren’t writing a check. When you get your statement, every month you’ll place a “√” through this box when you see the transaction listed.

- Service Fee: If you are charged a fee to withdraw money from the ATM, write that amount in this space.

- Deposit/Credit: Did you deposit money into your account or receive a credit from a merchant? Write down any deposit amounts into your account.

- Balance: To find out how much money you have, add the deposited money to what you had before. Or subtract the withdrawal amount from what you had before. The money left is your balance.

Automated Teller Machine (ATM): Also known as the money machine or cash machine.

Bad Check: A check that is written when there is not enough money in the account. Also known as a bounced check.

Balance: The amount of money you have in your account.

Cash: Money in the form of bills or coins.

Check: A document used for payment.

Check 21: Federal legislation passed in 2004 that permits financial institutions to create and submit substitute checks from electronic images for processing.

Check Register: A form to keep track of your checking account transactions.

Checking Account: A payment method to manage your money efficiently.

Cleared Check: A check that has gone through the financial institution’s processing center and is listed on your monthly statement.

Debit Card: A card that can be used at an ATM or merchant. Unlike a credit card, the funds are deducted from your checking account.

Deposit: The money you put into your account or the act of putting money into your account.

Deposit Ticket: The form you use to put money into your account.

Electronic Check: When you write a check to a merchant and the merchant hands the check back to you. The check is converted to an automatic deduction to your checking account.

Endorse: To sign your name on the back of a check in order to cash it or deposit it.

Financial Institution: An establishment that completes and facilitates money transactions, such as a bank or credit union.

Less Cash Received: The amount of cash you get back when you make a deposit.

Memo: The area on a check that notes what the check was written to pay for.

Non-sufficient Funds: When you do not have enough money in your account to cover a check, debit card purchase or other transaction.

Non-sufficient Funds Fee: The fee that is charged by a financial institution or business when a check does not clear or there isn’t enough money in your account to cover a transfer or withdrawal.

Outstanding Check: A check that is still going through financial institution processing.

Overdraft: When your account goes below zero and there is not enough money to cover the withdrawal.

Reconcile: A process to make sure your checkbook balance matches your financial institution’s balance for your account.

Reconciliation: When you have verified that your checkbook balance is the same as your financial institution’s balance for your account.

Reconciliation Form: A form that helps you reconcile your account. See Reconcile.

Recording a Transaction: The act of writing down a transaction in your check register. See Transaction.

Statement: The documentation you get every month from your financial institution that lists all of the activities in your account

for the month. Transaction: When money goes into, or out of, your account. Transactions can include deposits, withdrawals, payments, fees, ATM transactions or transfers.

for the month. Transaction: When money goes into, or out of, your account. Transactions can include deposits, withdrawals, payments, fees, ATM transactions or transfers.